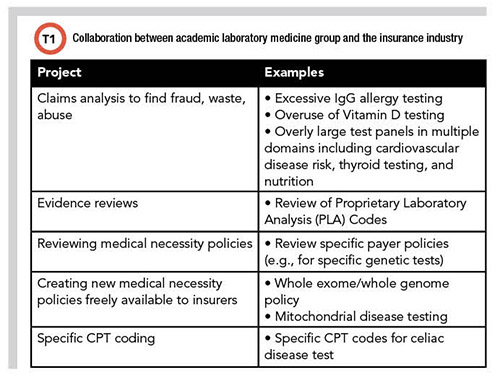

Mike Astion, MD, PhD, has been working in collaboration with insurers since he worked at the University of Washington in 2007. He brought that experience with him to Seattle Children's Hospital, which launched PLUGS in 2013. The partnership includes analyzing laboratory insurance claims, performing evidence reviews, creating or reviewing medical necessity policies, advocating for specific CPT coding over nonspecific codes, improving preauthorization for genetic tests, and explaining successful lab-payer collaborations through webinars and publications (Table 1). Astion, who cofounded the PLUGS program, is medical director of laboratories at Seattle Children's Hospital and professor of laboratory medicine and pathology at the University of Washington in Seattle.

How do the perspectives of payers, labs, and patients differ?

Payers focus on restricting payment to medically necessary tests, while clinical labs want fair payment for those tests. Patients want to avoid financial toxicity. As outlined in a recent article in CLN (October 2021), insurers and labs have multiple ways to reduce financial toxicity, recent federal and state laws and initiatives are addressing this issue.

What is meant by medically necessary, and how does cost play a role?

Medical necessity refers to a test needed to diagnose or manage a health condition. Medical necessity policies determine clinical criteria for a lab test to be a covered benefit. In general, payers base their definitions on peer-reviewed evidence. Since that is often lacking, they rely on guidelines based on research evidence and expert consensus.

Cost effectiveness is included in some medical necessity policies. More commonly, costs are unaddressed, and evidence is primary. Practically, costs matter! If genetic tests cost a dollar, insurance companies would not regulate them through administrative and medical necessity policies. All payers prioritize policymaking where money is wasted. Since waste is abundant, payers are rewarded for creating policies.

Importantly, administrative policies add another layer: They describe the requirements that the provider and patient must fulfill to access the medical necessity policy. This includes medical documentation as well as submitting an accurate, correctly coded claim. For certain genetic and other expensive tests, there are often additional administrative requirements related to preauthorization.

What are the economics of medical policy writing?

An example illustrates the financial return. If a payer spends $1 million annually on vitamin D testing and 20% is unnecessary, then the payer saves $200,000 through a vitamin D policy that denies unnecessary testing. The payer’s cost includes creating, maintaining, automating the policy in their claims system, and resolving patient grievances. This costs much less than $200,000. Many tests are similar to this example. Therefore, payers and third-party benefits managers actively manage testing.

How does this affect patients?

Policies are long and difficult to access and understand. There is no insurance industry standard on policy access, contents, and size.

It is challenging even to locate policies. Tests are rarely listed by name. For example, a specific tumor marker test may be inside a larger tumor marker policy, or in a genetic testing policy, but not searchable by the specific test name. Therefore, access often involves receiving help from the payer.

Moreover, policies contain medical vocabulary, so the patient requires help unless they have a medical education. Additionally, policies often are nonspecific about how scientific evidence links to coverage criteria.

Policies lack a simple summary, and their length is a challenge on its own. For example, a search of “tumor marker policy” for one insurer has >1000 references, covers 169 tumor markers if inclusion criteria are met, and denies >100 markers always. If there is potential coverage, it is hard to locate the pertinent policy section. In the pertinent section, it if difficult to discern if criteria are met.

How does PLUGS approach writing and reviewing medical necessity policies?

There are two aspects to the PLUGS approach. First, we provide guardrails against abuse without unduly blocking medical practice. Second, we allow wider guardrails for patients with severe illness.

Why not just require high-grade evidence? Because the US is not a single payer system with one interpretation of evidence. It is not realistic for physicians and labs to conform to differing views of multiple payers. Each payer cannot force a lab to practice that payer’s version of evidence-based medicine—a lab cannot dance simultaneously to that many kinds of music.

A guardrails approach is an answer to this problem. If insurers take a more generous approach to the evidence, and focus on guardrails that block abuse, then mainstream labs can succeed. Using an automobile analogy: a lab driving down the middle will usually not notice variations in guardrails.

In addition, broader guardrails should be given to specialists caring for severely ill patients. Patients with multiple medical conditions fit poorly into the categories covered by evidence. While it is never appropriate for these patients to experience laboratory quackery, it is fine for physicians to order a few more tests and monitor more frequently.

What is most challenging about developing medical necessity policies?

Guidelines and other expert opinions on utilization often are based on weaker grades of evidence, including consensus. We specifically try to avoid denying a test based on a lack of high-grade evidence when the standard of care is to provide that test.

This arises with older tests and panels used as markers of organ damage. For example, it is difficult to find guidelines on the frequency of monitoring patients who have diseases affecting multiple organs. When patients are extremely ill, the standard of care may require frequent monitoring with batteries of tests, but the peer-reviewed evidence for intense monitoring is limited.

Can you further compare the standard of care with evidence-based medicine?

This is a challenging aspect of insurance. The standard of care and evidence-based medicine are related but not identical. The standard of care refers to the expectations of a well-educated clinician to diagnose, treat, and monitor a condition. The standard of care is established through consensus among experts and is influenced by guidelines from professional and governmental organizations. Ideally, the standard is based on robust evidence, but often it is not. The standard of care is a clinical expectation, and violations are foundational to malpractice lawsuits. Therefore, insurance policies should support the standard of care.

Evidence-based medicine (EBM) uses scientific evidence to guide clinical decisions. For insurers, EBM involves evaluating research evidence to decide coverage. Insurers differ on the evidence level required for coverage, leading to coverage differences between payers.

PLUGS has a freely available exome/genome policy. With that policy, you did not begin with a wide guardrails approach. Why?

There are nuances to policy strategy. Our biggest success is the exome policy, which is now an exome/genome policy. When we started several years ago, insurers did not cover exomes and lacked a policy. Exome costs were thousands of dollars higher than common tests. Payers heavily considered cost. We realized we would be more successful starting with a policy with narrower inclusion criteria than that favored by our lab and PLUGS members. We focused on effectiveness rather than righteousness. Therefore, the approach to achieving coverage was to start slow and land something with a payer, then broaden the inclusion criteria as evidence strengthened. We were correct, and versions of our exome/genome policy now cover tens of millions of lives.

How do tests that begin as uncovered eventually become covered?

Insurers change from uncovered to covered because of four major factors: accumulation of independent evidence; new, favorable opinion in a national guideline; state or federal legislation; and patient grievances. Insurers dislike grievances because they represent dissatisfaction among customers.

Medical necessity policies are reviewed annually, offering a chance for a coverage change. If a national guideline newly supports coverage, it can still be a 3– to 12–month delay to incorporate into policy and program claims systems. During that delay, the patient is uncovered and pays the bill.

What is your future hope for medical necessity policies?

The hope is that there are more policies, and that they are based on guardrails to block abuse. They are easily accessible, short, and have a comprehensible summary. The policies are updated twice annually. The policies that produce the most denials would list the specific reason for denial.